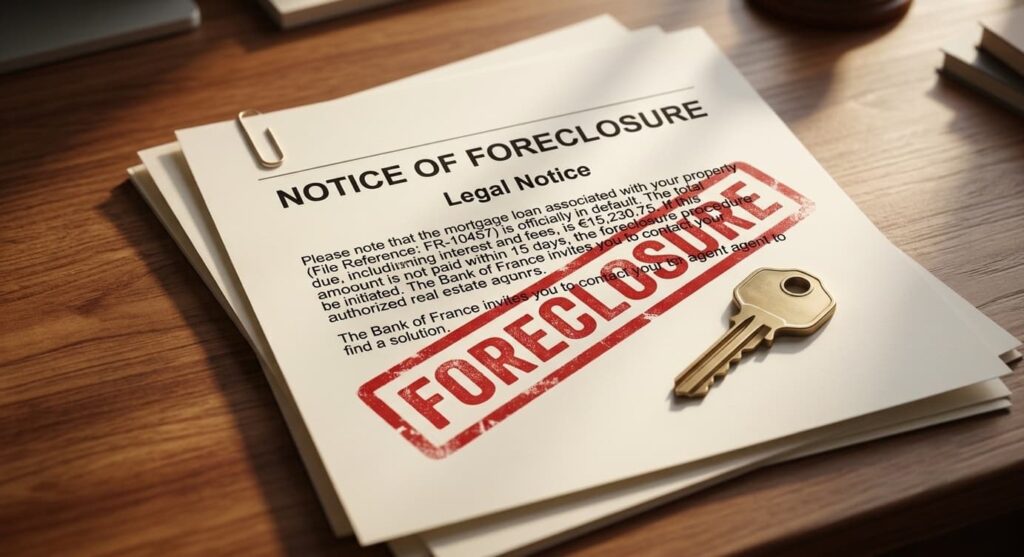

The 60-day notice: a warning sign to be taken seriously

A 60-day notice, also known as a notice of default, is one of the most serious warnings a homeowner can receive. In practical terms, the bank gives you two months to remedy a default situation, failing which it may seize and sell your home. The most common causes are:

- Late mortgage payments

- Lack of insurance on the property

- Improper use of the home (e.g., commercial use of a residential property)

Once they receive this notice, many homeowners panic and believe that the only solution is to sell their home. However, there are other options available. A well-structured private mortgage loan can give you the time you need to get back on track, pay off your urgent debts, and keep your home. The support of a specialized mortgage broker is essential, as they will be able to evaluate the options available to you based on your income, debts, and the equity in your property.

Legal mortgage for tax debts: an invisible danger

Few homeowners are aware that unpaid tax debts can lead to a legal mortgage. The Canada Revenue Agency (CRA) or Revenu Québec have broad collection powers. When they consider that all other options have been exhausted, they can register a tax lien on your home.

This measure does not directly result in the loss of your property, but it does reduce your financial flexibility. Your current or future lenders will see this lien and may refuse to refinance. Worse still, your institution may decide to call in the loan, forcing many homeowners to sell their property quickly.

What are your options for protecting your home?

Act quickly: the longer you wait, the more limited your options become.

- Private lenders often impose strict conditions when they perceive an emergency.

- Consult a mortgage broker: unlike private lenders, a broker regulated by the AMF is there to defend your interests and find the best strategy for your situation.

- Explore private refinancing solutions: these temporary loans are designed to get you out of a bind. Once your debts are paid off and your credit rating is restored, you can return to an institutional lender.

Why work with Mortgage Solutions?

At Mortgage Solutions, we have been supporting Quebec homeowners facing financial challenges for over 10 years. Our team is certified by the Autorité des marchés financiers (AMF) and has a network of reliable lenders.

We understand that behind every legal mortgage or 60-day notice, there is a family and a life plan to protect. That’s why we implement quick, humane solutions tailored to your situation.

Call us now at 1-888-708-5576 or fill out our online form.

A quick consultation can make all the difference.